The B2B2x value chain is being rebuilt from the inside out

How digital infrastructure and AI are reshaping every stage of embedded and affinity insurance programme design.

The B2B2x insurance model has always been structurally attractive. A distribution partner with an established customer base. An insurer or MGA with the product and capacity. A technology layer connecting them. Revenue flowing to all three parties when the programme performs.

What is changing — rapidly — is what "the technology layer" means. For most of the past decade, that phrase described an API connection and a white-label policy document. Today it describes a full-stack digital infrastructure that is disrupting how programmes are priced, distributed, converted, serviced, and economically structured. The disruption is not uniform across the chain. It is concentrated at specific nodes, and understanding where it is happening — and what it means for programme design — is the starting point for building programmes that can compete over the next five years.

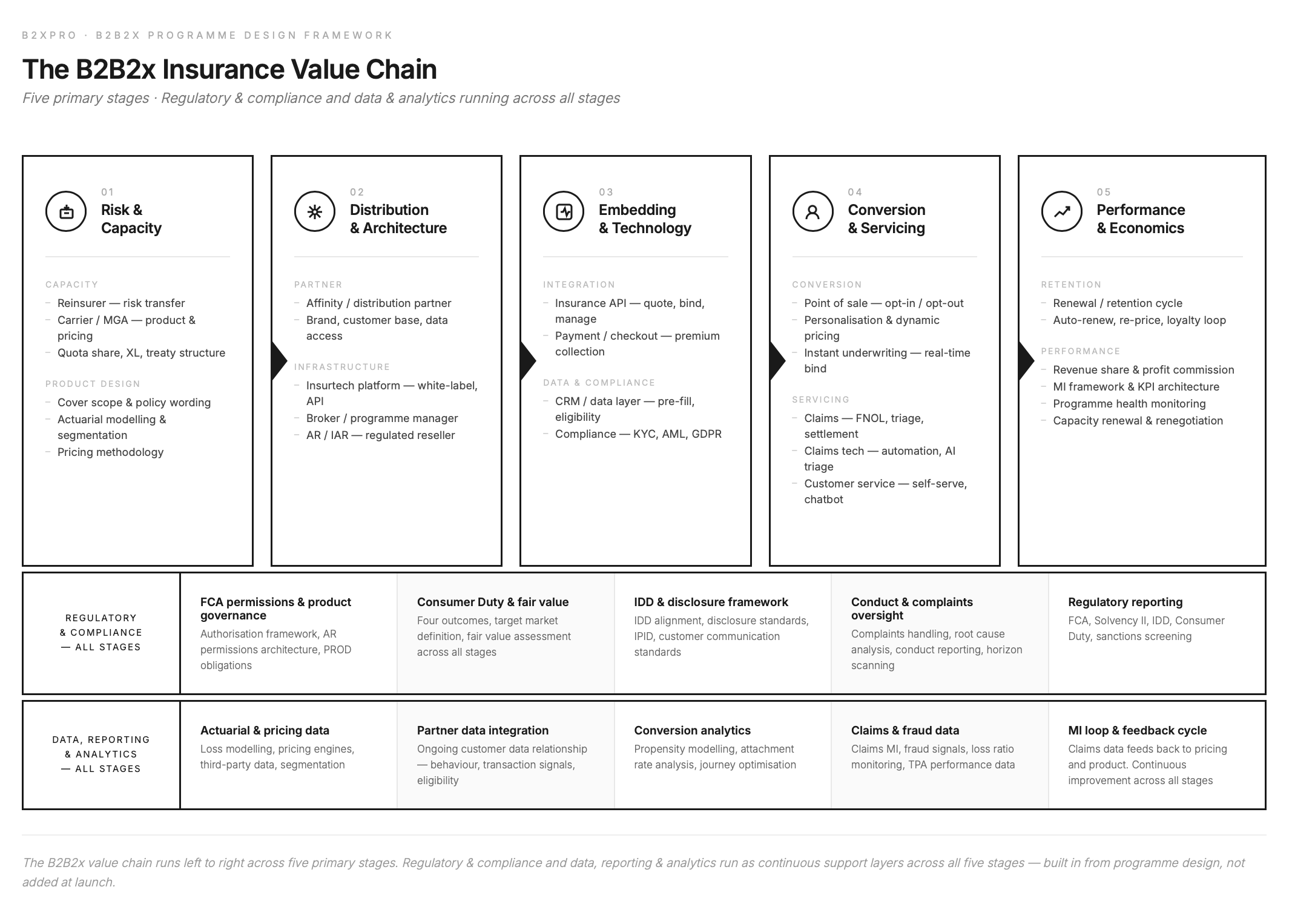

This article maps that disruption across the five layers of the B2B2x value chain.

Risk and product: the capacity layer is opening up

At the top of the chain, the reinsurer-carrier-MGA structure is being transformed by data. The traditional model — a carrier or MGA pricing a product based on historical loss data, submitted to reinsurers on an annual treaty basis — is giving way to something more dynamic.

Actuarial and data capabilities that once lived exclusively inside large carriers are now accessible to MGAs and programme managers through third-party data platforms, pricing engines, and modelling tools. A well-structured MGA can now bring actuarial sophistication to a niche programme that five years ago would have required a full carrier relationship to underwrite credibly.

For programme designers, this matters because the product design conversation is no longer constrained by what a carrier's existing pricing model can accommodate. Cover scope, segmentation, pricing methodology — all of these can be built around the distribution partner's customer data rather than backward from a carrier's book assumptions.

The regulatory layer at this stage — authorisation, rules, capital requirements — has not changed in character, but the FCA's increasing focus on product governance and fair value means that the data infrastructure built here must also support the reporting and oversight obligations that run through every subsequent stage.

Distribution: the intermediary layer is consolidating and specialising

The distribution layer — affinity partner, insurtech platform, broker or programme manager, AR network — is where the structural architecture of a B2B2x programme is established. This is where the regulatory permissions are allocated, where the commercial relationships are governed, and where the white-label or co-brand decision is made.

The digital disruption here is not replacing the intermediary layer — it is changing what a capable intermediary looks like. Insurtech platforms now provide the API infrastructure, white-label presentation, and compliance tooling that previously required a full MGA or broker build. Programme managers who previously competed on relationships now need to compete on technical capability as well.

For programme design, the implication is that the choice of distribution architecture — who holds what permissions, how the AR or introducer structure is configured, what the insurtech layer does — needs to be made with a clearer view of the digital infrastructure requirements than was necessary even three years ago. Getting this wrong at the distribution layer creates structural problems that cannot be fixed at the embedding or conversion stage.

Embedding: the integration layer is the new competitive moat

The embedding layer — insurance API, payment and checkout integration, CRM and data layer, compliance infrastructure — is where the programme is built into the distribution partner's environment. This is the stage that most directly determines whether an embedded insurance programme feels like a natural part of the partner's product or an awkward bolt-on.

The quality of the API integration determines the customer experience at point of sale. The CRM and data layer determines what the programme knows about each customer — their eligibility, their prior behaviour, their propensity to buy — and therefore how well the programme can personalise and pre-fill the purchase journey. The compliance infrastructure — KYC, AML, GDPR — needs to be woven into the embedding layer rather than applied as a checkpoint at the end.

The shift here is from integration as a one-time technical project to integration as an ongoing data relationship. The programmes that are pulling away from the field are those where the insurer or MGA has genuine access to partner data — not just at point of sale, but continuously — and can use that data to improve pricing, reduce friction, and sharpen the customer proposition over time.

Conversion: where GenAI and machine learning are having the most immediate impact

The conversion layer — point of sale, personalisation, instant underwriting, end customer — is where the disruption is most visible and most commercially significant right now.

Instant underwriting — rules engines that bind cover in real time, with no forms and no human intervention — is no longer a differentiator. It is a minimum requirement. The question is no longer whether a programme can bind instantly. It is whether it can bind intelligently — using propensity modelling, dynamic pricing, and pre-fill to present the right cover at the right price to the right customer at exactly the moment they are ready to buy.

This is where GenAI and predictive machine learning are genuinely changing what is possible. Hyper-personalisation at scale — presenting a product that feels tailored to an individual customer's situation, behaviour, and context, without requiring that customer to answer a series of questions — is now within reach for well-structured programmes that have built the data infrastructure to support it.

The commercial consequence is significant. Attachment rates on programmes with strong personalisation and low-friction journeys are materially higher than those relying on static opt-in widgets and generic pricing. In a B2B2x model where the distributor's primary motivation is revenue generation, the difference between a 4% and an 8% attachment rate is the difference between a programme the partner actively promotes and one they deprioritise.

The point of sale design — opt-in vs opt-out, bundled vs purchased separately, the moment of offer within the customer journey — remains as important as ever. But the intelligence behind that design is what separates programmes that perform from those that plateau.

Servicing: automation is raising the floor on claims and retention

The servicing layer — claims handling, claims technology, customer service, renewal and retention — has historically been the stage most resistant to digital transformation. Claims are complex, emotionally charged, and legally governed. Getting them wrong is expensive in every direction.

That is changing. Claims automation, AI triage, and chatbot-assisted customer service are compressing the cost of handling high-frequency, low-complexity claims while improving the customer experience. FNOL — first notification of loss — is increasingly digital and immediate. Triage is increasingly automated. Settlement on straightforward claims is increasingly instant.

For programme designers, the implication is that the claims operating model needs to be specified at programme design stage, not bolted on at launch. The choice of TPA, the delegated claims authority framework, the service level standards — these need to reflect what the digital servicing infrastructure can deliver, not what was standard practice five years ago.

On retention, seamless auto-renewal combined with dynamic re-pricing — adjusting the renewal offer based on claims history, engagement data, and market conditions — is materially improving retention economics on programmes that have built the data infrastructure to support it. Programmes that still treat renewal as an annual administrative event rather than a managed commercial cycle are leaving significant value on the table.

Economics: the feedback loop is the prize

The economics layer — revenue share, data and analytics, regulatory reporting — is where the long-term value of a well-designed B2B2x programme is realised or lost.

Revenue share and profit commission structures that align incentives across all three parties — insurer, programme manager, distribution partner — are the foundation. But the real economic prize in a digitally mature B2B2x programme is the data and analytics loop.

Claims and loss data, re-pricing signals, fraud detection, and customer insight — generated continuously by the live programme — feed back into product design, pricing, partner positioning, and customer proposition. Programmes that build this feedback loop from day one compound their advantage over time. Those that treat MI as a reporting obligation rather than a strategic asset fall progressively further behind.

Regulatory reporting — FCA, Solvency II, IDD, Consumer Duty, sanctions screening — runs as a continuous obligation across all stages. The digital infrastructure that supports the analytics loop, when properly designed, also supports the regulatory reporting obligation. The two are not in tension. They draw on the same data.

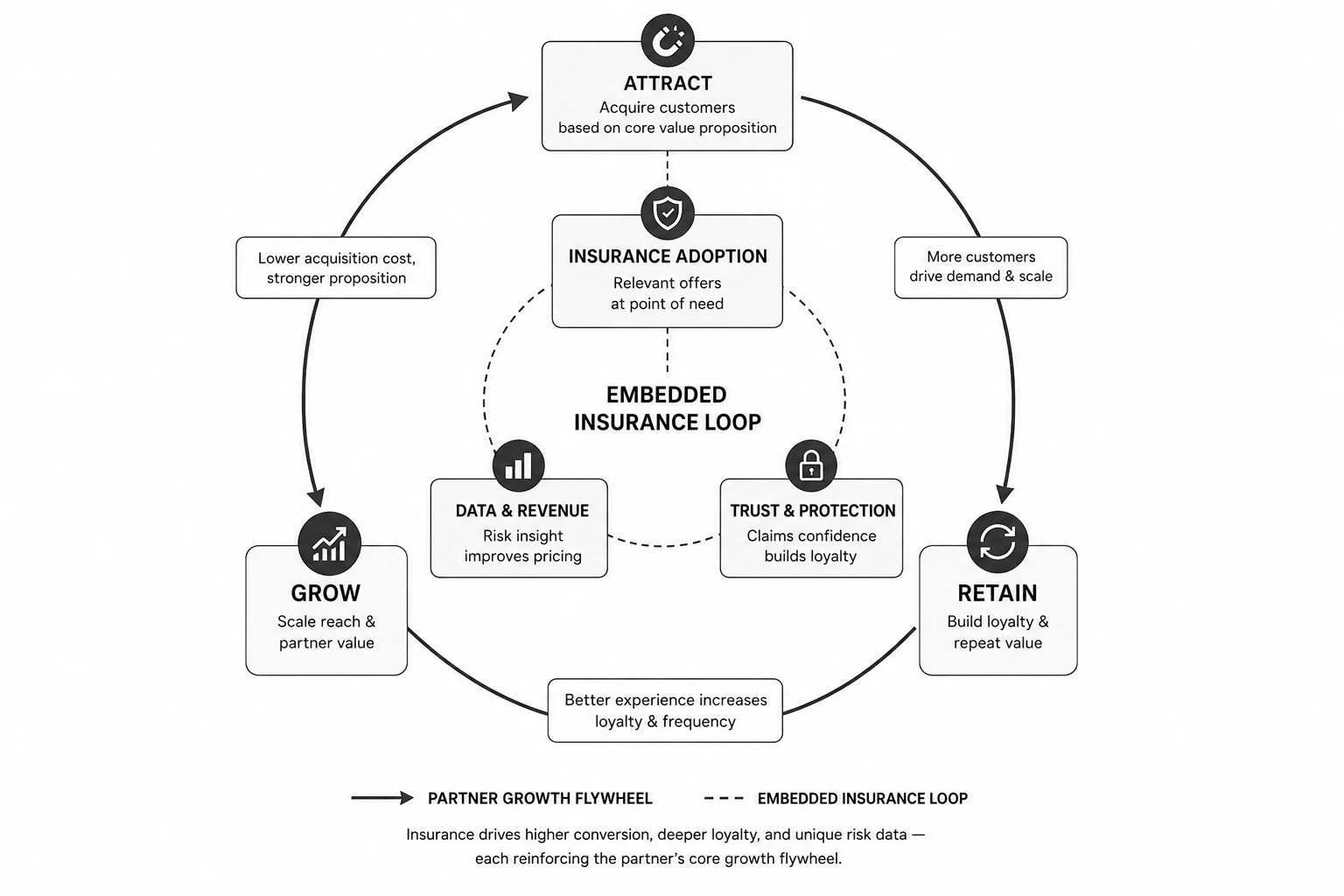

The B2B2x embedded insurance flywheel - How embedded insurance strengthens every stage of the partner growth loop.

What this means for programme design

The B2B2x value chain is not being replaced by digital technology. It is being upgraded by it. The parties, the relationships, and the regulatory framework remain fundamentally the same. What is changing is the infrastructure that connects them and the data that flows through it.

For anyone designing or reviewing a B2B2x programme today, the questions this raises are concrete:

Where in the chain is the data relationship owned, and by whom? Is the embedding layer built for ongoing data access or one-time integration? Does the conversion design reflect what personalisation technology now makes possible, or is it based on what was standard three years ago? Is the claims model designed for digital servicing from the outset, or retrofitted? And does the economics structure incentivise all parties to invest in the data infrastructure that makes the programme improve over time?

These are not technology questions. They are programme design questions. The technology is available. The question is whether the programme is structured to use it.

B2XPRO is a specialist management consultancy working across the full B2B2x insurance value chain — from programme design and capacity strategy through to performance management. We do not arrange, sell, administer, or advise on insurance contracts and do not carry on regulated insurance distribution activities.